SCAA Newsletter - 1/10/21

SCAA Newsletter - 1/10/21

Part 2 - How the stock market affects card prices

Welcome back to this week’s SCAA Newsletter, where I will conclude last week’s discussion about comparing returns between card prices and the S&P 500. Last week, we looked at the PWCC 100, which is a list of the 100 most valuable frequently-traded vintage cards in the hobby and has outperformed the S&P 500 substantially since 2008. This week, I will show you why that can be a misleading barometer to use when comparing the attractiveness of investing in vintage sports cards versus public stocks.

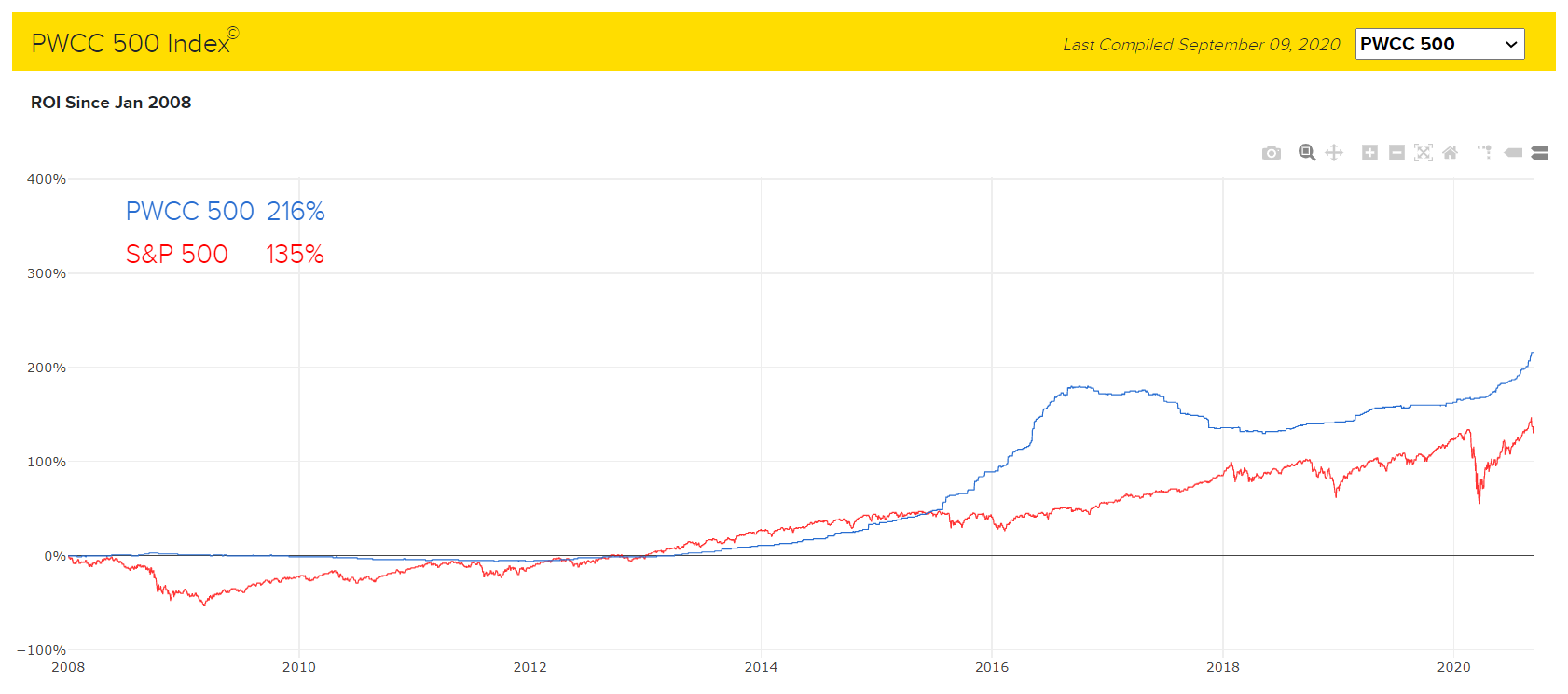

PWCC 500

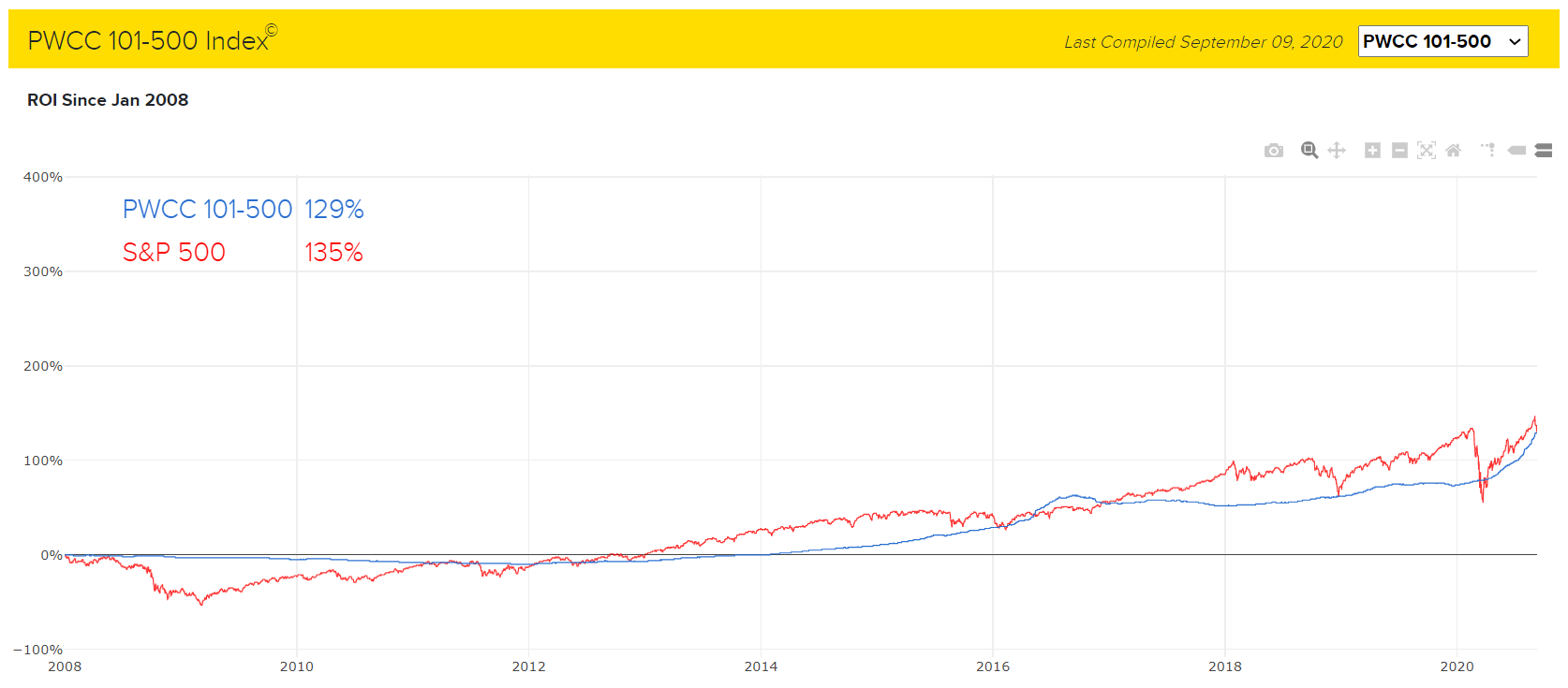

The top chart shows the PWCC 500, which has outperformed the S&P 500 materially since 2008, while the bottom chart shows the PWCC 101-500 Index, comprised of the cards in the PWCC 500 that fall outside of the top 100 most valuable cards, which has been roughly in line with the performance of the S&P 500.

As mentioned in a prior newsletter, you have to think about investment return as a compensation for risk. A key risk that is especially applicable to sports cards is illiquidity. In order to be appropriately compensated for this risk, the investor should be getting a return for his illiquid assets in excess of a return he could get for liquid assets because if he doesn’t, he could just invest in liquid assets and have flexibility to enter/exit at his choosing without sacrificing any return.

What does the illiquidity premium have to do with the charts above? It means that a return in line with the S&P 500 isn’t good enough. You need a return in excess of the returns achievable by the public markets in order to make investing in sports cards worth your while from an investing standpoint.

Although the PWCC 500 has exceeded the returns from the S&P 500 over this timeframe, the key insight here is that outperformance is hugely driven by the top 100 cards in the index. When just investing in cards 101-500, you are only in line with public markets, which is not worth the additional risk you take on as an investor for dealing with illiquid assets. This is a completely different story than what you would think when seeing the hype around the card industry.

This doesn’t mean cards are a bad investment. It just means that buying a vintage card, even if it is among the top 500 most valuable cards in the entire hobby (which has produced millions of cards in its history), is not a guaranteed ticket to a good investment. Vintage cards commonly have the reputation of being “safe” investments that have locked-in their value because they will only continue to get older and more scarce, leading them to appreciate in value. That is not true. A card might get more valuable over time, but if that appreciation does not outpace the increase in value of its public benchmark (i.e. the S&P 500 in this case), it is an unattractive investment because you would have been better off just putting your money in a S&P 500 ETF and having greater liquidity.

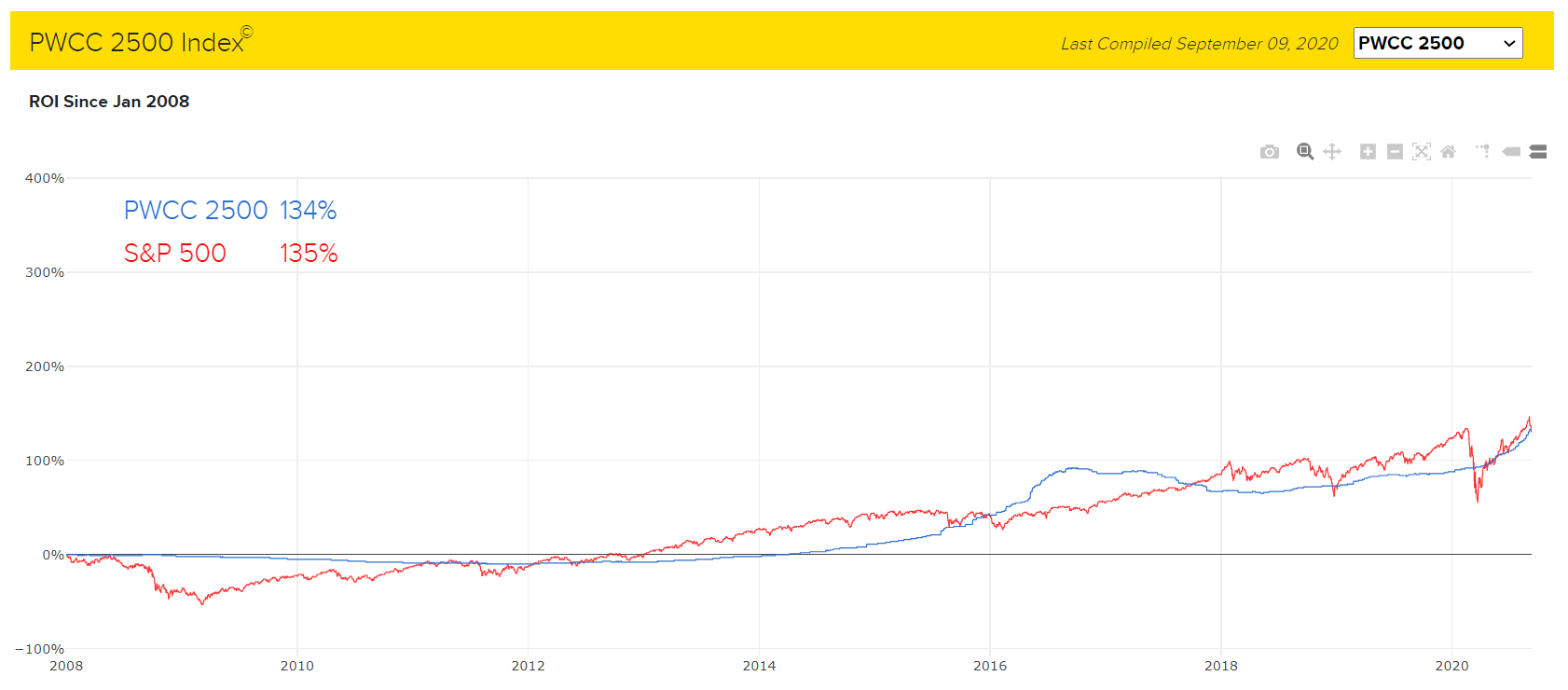

PWCC 2500

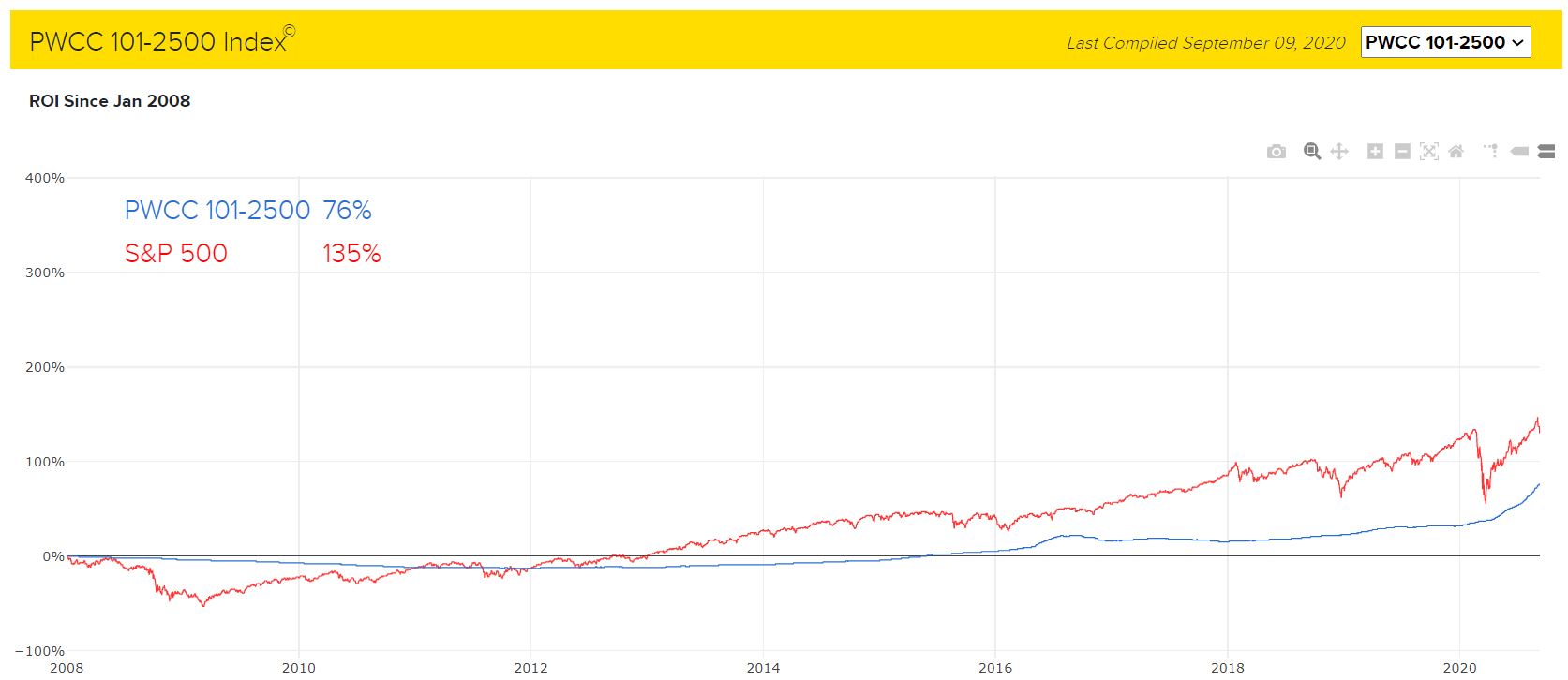

Unsurprisingly, this trend continues when expanding the index to the top 2500 cards in the hobby. The PWCC 2500 is basically in line with the S&P 500 over this timeframe, but when you remove the top 100 cards (only 4% of the index), that return plummets to trailing its benchmark by ~60%. That is an enormous difference that is driven entirely by the assets at the very top of the hobby.

This is not meant to scare you away from investing in vintage cards. It is simply to dispel the notion that you can just throw money at vintage cards for consistent returns in your portfolio. In the same way you have to scout a prospect who you are considering investing in who hasn’t played above Double-A, you need to evaluate the future return potential of players whose careers ended decades ago.

Takeaways

Vintage cards are not guaranteed to drive returns in your portfolio

Eddie Collins is in the top 10 of all-time WAR. He is a Hall of Famer. He had over 3000 hits and was a 6x World Series champion. He was a member of the 1919 Black Sox team, which remains one of the most notable teams in baseball history. Despite all of that, his t206 cards are extremely affordable compared to many others and, likely, what his career should justify. Why did that happen? Frankly, I don’t know (I’m sure the high pop of his t206 card has a little to do with it, but he’s still much rarer than Cobb). Regardless of the reasons, the reality is that he is a player who doesn’t have the same collecting prestige as other players from his era in the hobby, despite an incredible career on great (and notorious) teams.

I am a big believer in the value of vintage cards and they comprise a substantial proportion of my own portfolio, but Collins is just one example of how difficult it can be to predict hobby interest in a player, despite his checking boxes that may seem obvious to trigger collector interest. No matter how great a player’s stats are or how old a card is, due diligence on investing in a card is always paramount, regardless of the card’s era.

Tail events drive card returns, as they do for many other assets

The Psychology of Money by Morgan Housel is one of my favorite books I’ve ever read about investing and personal finance. If you have not read it, I would strongly recommend checking it out. A key point reinforced throughout the book is how much tail events drive basically everything in investing. An example from the book that drives that point home is below (emphasis is my own):

J.P. Morgan Asset Management once published the distribution of returns for the Russell 3000 Index - a big, broad collection of public companies - since 1980. Forty percent of all Russell 3000 stock components lost at least 70% of their value and never recovered over this period. Effectively all of the index’s overall returns came from 7% of component companies that outperformed by at least two standard deviations.

This exact same concept happens in these PWCC Indices. You would think that vintage cards are stable. You would think that they are so rare and old that they have to be valuable. You would think that the top 2500 vintage cards, in an industry that has produced millions, would be so sought-after that they would outperform a diversified stock index easily. But elite vintage sports cards are the same as many other concepts in finance - they are driven by tail returns. The very best-of-the-best, the PWCC 100, is responsible for effectively all outperformance of vintage sports cards over a 12-year period. This means that the higher value the card, the better your chances are that it will lead to outperformance.

This would seem to support the concept of investing through fractional services like Rally, just so long as you are doing so to access absolutely best-of-the-best cards that would comprise this group of return-drivers for the entire industry. Additionally, regardless of your investing platform, this concept puts further emphasis on valuing quality above all else when considering cards for inclusion in your portfolio.

Thanks for reading this week’s newsletter. Please subscribe/share below and if you ever have any questions, comments, or requests for future newsletters, reach out to @SportsCardAA on Twitter.

Disclaimer - the insights found in this newsletter or any other content provided by SCAA do not constitute investment advice. Investors are encouraged to conduct their own research.